Tomorrow, Jerome Powell chairs his final FOMC meeting as Fed Chair. The rate decision is not the story. The metal at $4,713 has already told you what the story is.

Powell's Last Meeting: What Gold Already Knows About the Warsh Era

Sound Money Weekly | April 27, 2026

The Hook

There is an old saying in markets: when the expected happens and the price moves the wrong way, pay attention.

On April 24, the Department of Justice dropped its criminal probe of Fed Chair Jerome Powell. Within hours, Kevin Warsh's confirmation odds on Polymarket jumped from 27% to 85%. Warsh is a known inflation hawk. A hawkish Fed successor means higher real yields. Higher real yields mean lower gold. Every model pointed the same direction.

That backward move contains more information than any rate decision will tomorrow. The market had not been pricing the rate path. It had been pricing something deeper: the risk that Washington's executive branch could subordinate the Federal Reserve to political pressure. When the DOJ probe hung over Powell, every foreign central bank on earth watched to see whether the Fed's independence was real or just institutional theater. When that question was finally answered -- the probe dropped, Warsh on a clear confirmation path -- gold did not react to the hawkish rate implications. It exhaled.

Sound money does not fear a credible Fed. It fears the alternative.

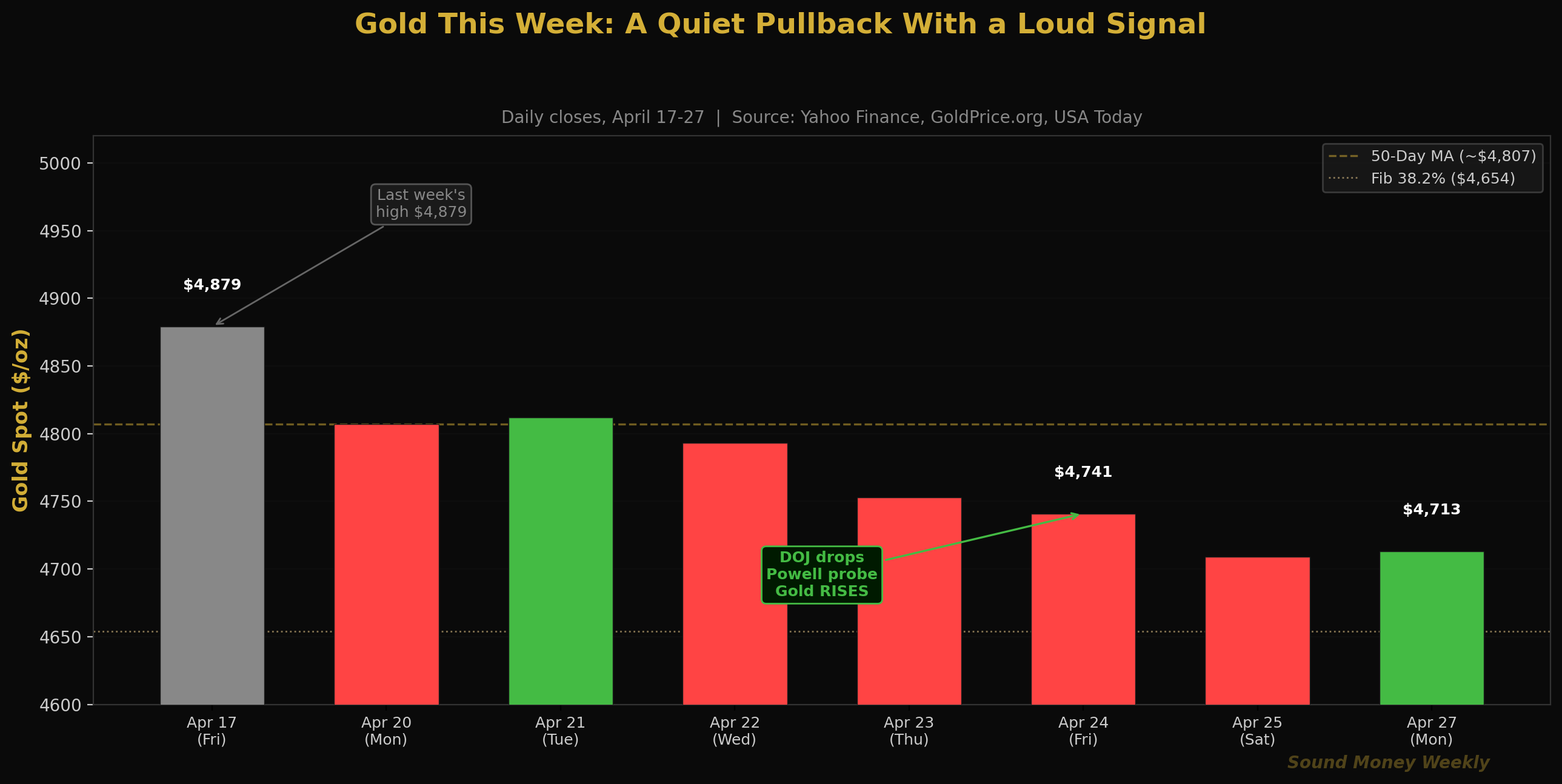

This week, gold pulled back modestly to $4,713 as markets digested four simultaneous developments: the Warsh transition, Powell's approaching final meeting, Iran ceasefire extension, and silver's giveback of last week's gains. The price action was quiet. The structural signal was anything but.

At $4,713 gold trades 16% below its January all-time high and 40.5% above where it was a year ago. Every major bank still projects $5,400 to $6,300 by year-end. And tomorrow, the man who has chaired the Fed through its most inflationary period in four decades steps to the podium for the last time.

The Week in Full

Monday-Tuesday, April 20-21: Gold opened the week near $4,807 -- essentially flat -- as the Warsh Senate hearing began. Markets expected dramatic price moves given the implications for monetary policy. They did not come. Gold at $4,809 on April 20 was, as GoldSilver.com noted, "barely moved" during the most consequential Fed confirmation hearing in years. That calm was itself a signal: the institutional bet on gold was not a bet on one chair or one rate path. It was a bet on the underlying monetary environment.

Wednesday, April 22: Silver intraday surged above $78.67 -- a +4.2% single-session move that briefly crossed the threshold. Catalyst: Trump extended the Iran ceasefire combined with the Warsh hearing's hawkish overtones driving a simultaneous safe-haven bid. Silver closed at $78.45 (+1.06%) as the intraday premium faded.

Thursday-Friday, April 23-24: The DOJ dropped its criminal probe of Powell on April 24. The probe had centered on renovation cost irregularities at Fed buildings -- but its real significance was the question it posed: would a US president use law enforcement to discipline an independent central bank? When US Attorney Jeanine Pirro, who had said just days earlier that "this investigation continues," abruptly closed the case, prediction markets repriced Warsh's confirmation odds to 85%. Gold rose. The dollar fell. Markets had been discounting Fed credibility -- and credited it back the moment the threat cleared.

Gold closed Friday at approximately $4,741. Down for the week from last week's $4,879 high, but up from Thursday's intraday lows.

Weekend and Monday open: Gold at $4,713 as markets enter FOMC week in "wait and see" mode. Yahoo Finance's morning report describes investors as "cautious" ahead of the Fed meeting, with gold futures opening -0.6% from Friday's close.

Silver: Giving Back the Surge

Silver's 12.1% surge from April 11-17 was always likely to face some consolidation. This week delivered it: silver fell approximately 6.3% to $75.79 by Friday's close, giving back roughly half of last week's gains. The gold-silver ratio widened from 59.6:1 back toward 62:1.

This is not a structural break -- it is the normal oscillation of a more volatile metal. The Silver Institute's 67 million ounce deficit projection for 2026 and the ongoing industrial demand from solar, EVs, and AI infrastructure have not changed. Keith Neumeyer, CEO of First Majestic Silver, described the pullback as "market consolidation, not a structural break", noting that silver miners are generating record cash flow at current prices.

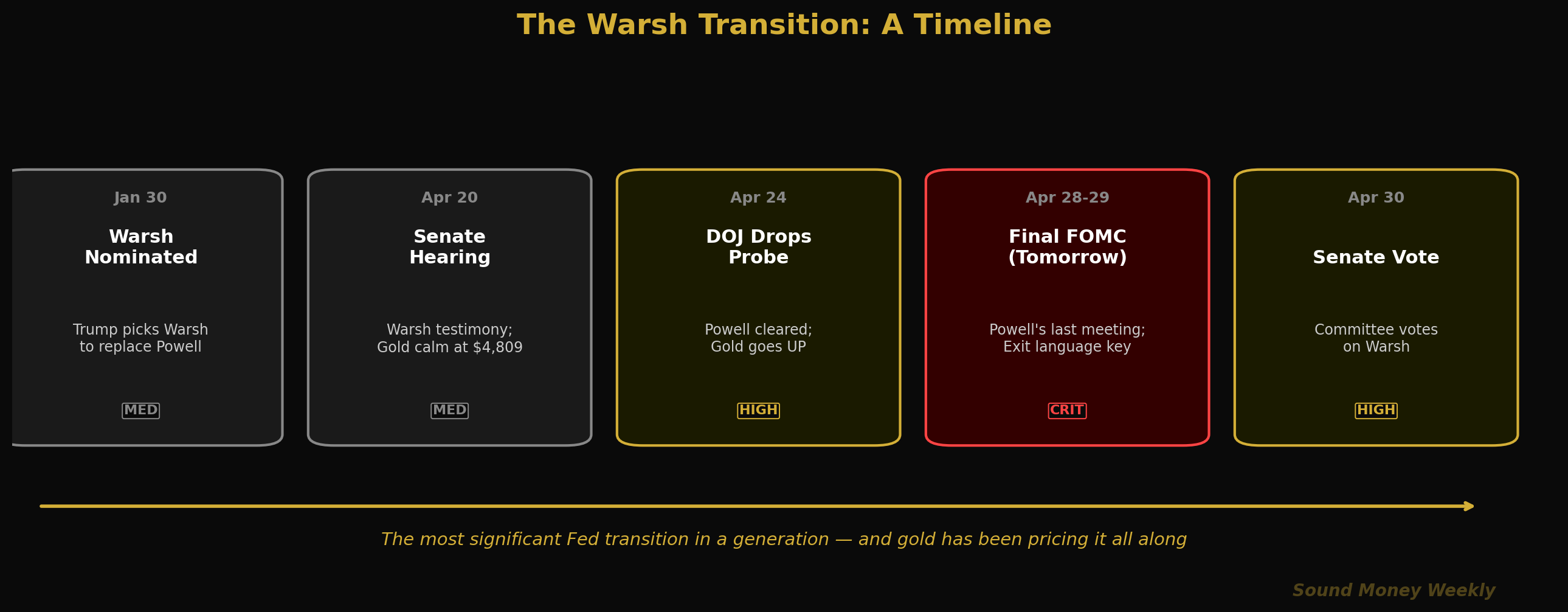

The Warsh Transition: A Timeline

The sequence of events over the past three months has been a compressed version of one of the most consequential Fed transitions in a generation:

- January 30: Trump nominates Kevin Warsh to replace Powell

- April 20: Senate Banking Committee hearing; gold barely moves despite hawkish testimony

- April 24: DOJ drops Powell probe; Warsh confirmation odds jump to 85%; gold rises

- April 28-29 (tomorrow): Powell's final FOMC meeting; rate hold near-certain (99.5% per CME FedWatch); exit language is the real variable

- April 30: Senate Banking Committee votes on Warsh confirmation

- May 15: Powell's term as Fed Chair expires; Warsh takes over

The rate hold tomorrow is, as Marcus Holt analyzed, "a mathematical inevitability." The real question embedded in the meeting is what Powell says on his way out the door. Does he signal any openness to rate cuts if energy prices fall and Iran pressure eases? Or does he preserve the hawkish ceiling and leave it to Warsh to decide?

Either way, one fact sits underneath all of it: five consecutive FOMC meetings have featured at least one dissenting vote -- a level of internal division not seen in over 36 years. The institution Warsh is inheriting is not unified. It has not been unified since October. And as Morgan Stanley's chief economist noted, rate cuts are still "scheduled" -- just assigned to new management.

Under the Hood: The Technical View

For readers who want the levels and data. For the plain-English takeaway, skip to "What It Means."

Gold: Holding the Recovery

Gold at $4,713 this morning remains:

- 16% below the January $5,608 all-time high

- 15% above the March 23 flash-crash low of $4,098

- Above the critical Fibonacci 0.382 level at $4,654 (reclaimed during the ceasefire bounce and holding)

- Just below the 50-day moving average at approximately $4,807

| Level | Price | Status |

|---|---|---|

| 50-Day MA (resistance) | ~$4,807 | Overhead target; was briefly exceeded April 17 |

| Fib 0.382 (support) | $4,654 | Holding as support after being reclaimed |

| Current | $4,713 | Between the two; consolidation zone |

| Fib 0.500 (major support) | $4,361 | Far below; structural floor intact |

| 200-Day MA | ~$4,200 | Long-term bull/bear line; not a concern |

A dovish Powell exit statement tomorrow -- any signal that rate cuts are on the 2026 horizon -- could send gold quickly back toward $4,807 and test the 50-day MA. A hawkish exit reinforces the near-term ceiling. Watch the post-meeting press conference.

The Structural Argument That No Fed Chair Can Override

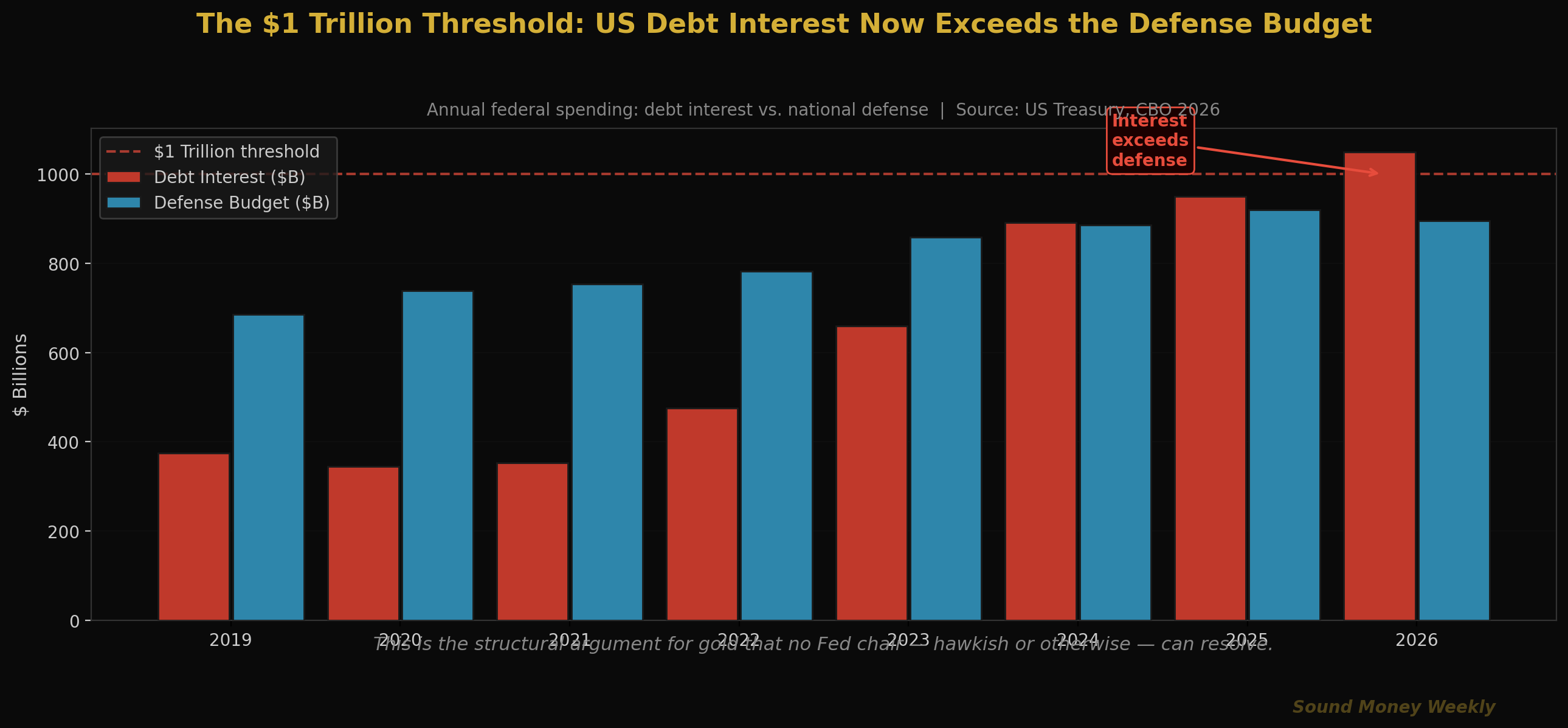

This is the data point that the Warsh rate debate obscures. In fiscal year 2026, the United States will pay more than $1 trillion in interest on its federal debt -- surpassing the defense budget for the first time in American history. The total federal debt sits near $39 trillion, with $9.2 trillion in Treasury debt maturing this fiscal year alone and needing refinancing at current elevated rates.

This is not a rate policy question. It is a structural question. No Fed chair -- however hawkish -- can credibly tighten monetary conditions enough to meaningfully erode a $39 trillion debt load without triggering a debt spiral. The Volcker option that broke inflation in 1982 is arithmetically unavailable in 2026. Rates high enough to truly discipline inflation would produce debt service costs that would themselves be inflationary through deficit financing.

This is what gold is pricing. Not Kevin Warsh specifically. Not any single rate decision. The mathematical constraint that makes eventual debasement the path of least resistance regardless of who chairs the Fed.

The DCA Math This Week

Gold at $4,713 this morning remains 16% below the January all-time high. The math is consistent with what we have been tracking throughout the recovery:

| Entry Point | Price | Oz per $200 | Value at Goldman $5,400 target |

|---|---|---|---|

| January ATH | $5,608 | 0.03566 oz | $192 |

| Today | $4,713 | 0.04243 oz | $229 |

| March low | $4,098 | 0.04881 oz | $264 |

At today's price, every $200 monthly purchase acquires 0.04243 ounces -- 19% more metal than the same purchase at January's all-time high. Over 12 months at this price, consistent $200/month stacking accumulates approximately 0.509 ounces. At Goldman's $5,400 year-end target, that becomes $2,749 -- a 14.5% return on $2,400 invested. At Wells Fargo's $6,100 target, it's $3,107 -- a 29.5% return.

The people who have been stacking consistently through this cycle -- buying at $5,000 and $4,700 and $4,400 and $4,100 -- have accumulated gold at an average cost well below today's price. The people waiting for clarity before restarting are buying at today's prices. The math does not change based on who chairs the Federal Reserve.

The investors who built wealth through gold's 1,075% total return since 2000 were not the ones who studied Fed transition timelines. They were the ones who kept showing up. The winners in this game are always in the game.

What It Means

Here is the plain-English version.

Gold's most important data point this week was not the price -- it was the direction. When the DOJ dropped the Powell probe and Warsh's path cleared, gold should have fallen by every conventional model. A hawkish successor + a credible confirmation path = higher real yields = lower gold. Instead gold rose from its intraday lows of $4,689 to close near $4,741. That move means markets had been pricing something beyond the rate path: the risk that the Fed's institutional independence was compromised. When that risk cleared, gold credited it. Sound money does not fear a credible Federal Reserve. It prices the risk of an incredible one.

The structural case has not changed. US debt interest exceeds $1 trillion annually for the first time in history, surpassing the defense budget. $9.2 trillion in Treasury debt needs to be refinanced this fiscal year at elevated rates. No Fed chair -- Warsh or any successor -- can make that math disappear. Goldman Sachs, J.P. Morgan, Wells Fargo and UBS all maintain year-end gold targets of $5,400 to $6,300. Not one has cut after a 16% drawdown from the ATH.

Tomorrow is Powell's last meeting. The rate decision is settled. The question is what his exit language signals about the path for cuts -- particularly if Iran tensions ease and oil retreats from $100. A constructive statement could send gold back toward $4,807 quickly. The subsequent Warsh era begins with markets watching whether the new chair softens on balance sheet reduction. Either signal could be a near-term catalyst.

At $4,713, you are still buying discounted metal. Gold is 16% below the all-time high. Each monthly purchase acquires 19% more ounces than the same purchase in January. The structural drivers -- central bank accumulation at a projected 850+ tonnes this year, fiscal deficits that compound regardless of political leadership, the silver supply deficit entering year six -- have not resolved. They have only grown more entrenched.

This is not a recommendation. We lay out the data, hear all sides, and tell you what we think. We think the Warsh transition is the most significant institutional event for gold since the Fed's 2021-22 policy error created the inflation that gold has been pricing ever since. We think the structural case for consistent accumulation is stronger now than it was before the March selloff. And we think the people positioned before the transition captures the structural move -- not those who begin positioning after the new chair takes over.

What We're Watching

Tuesday, April 28 - Wednesday, April 29: FOMC meeting and Powell press conference. The rate decision is not the story. Watch Powell's exact language on the rate path, the balance sheet, and the Iran/oil-driven inflation outlook. Any softening toward cuts -- even coded language -- could compress real yields and give gold a short-term lift heading into the Warsh era. A hawkish exit reinforces the near-term ceiling near $4,807.

Wednesday, April 30: Senate Banking Committee votes on Warsh. The final procedural hurdle before a full Senate vote. With Sen. Tillis dropping his blockade and Polymarket at 85% odds, the market has largely priced confirmation. Watch for any unexpected hold or procedural delay -- a vacuum at the Fed chairmanship would itself be a gold signal.

May 15: Powell's term expires. Even if Warsh is confirmed, the handover date is the next institutional marker. Powell has indicated he would serve as "chair pro tem" if needed -- but that transitional ambiguity is itself a structural argument for hard assets.

The $4,654 level. The Fibonacci 0.382 retracement. As long as gold holds above this level, the recovery structure from the March flash crash remains intact. A break below puts the bull thesis in question. It has held through every test since the ceasefire bounce. Watch it closely this week.

Silver's GSR. The gold-silver ratio widened from 59.6:1 back toward 62:1 this week. If it compresses back toward 57:1 -- the February 2026 low -- silver is historically in a breakout zone. The structural deficit story has not changed; only the short-term momentum has.

Until Next Week

Tomorrow Jerome Powell walks to that podium for the last time. He inherits a Fed that has 5 consecutive meeting dissents, $9.2 trillion in debt to refinance, oil above $100, and an institution whose independence was publicly questioned by the executive branch for the first time in a generation.

The metal at $4,713 has already priced all of it.

The rate hold will be unanimous. The press conference will be measured. And somewhere in Powell's exit language -- in what he says about the path to cuts, in what he acknowledges about the limits of Fed independence against a $39 trillion debt load -- gold will find its next signal.

For the people who have been stacking through this cycle, none of this changes the calculus. You do not need to predict what Powell says tomorrow, or how Warsh will govern, or when Iran resolves. You need to understand the structural argument. US debt service exceeds defense spending for the first time in history. Central banks bought gold for the 17th consecutive year. Silver's sixth annual supply deficit approaches. Each $200 purchase today acquires 19% more gold than the same purchase at the January high.

The structural case compounds quietly while markets obsess over the short-term signals. The winners in this game are always in the game. See you next Monday.

Sound Money offers fractional gold and silver ownership at whole-ounce pricing -- no minimums, no premiums. Learn more at sound.money.

Disclaimer: This content is provided by Sound Money for educational and informational purposes only. Nothing published here constitutes investment advice, financial advice, trading advice, or any other form of professional advice. Sound Money is not a registered investment advisor, broker-dealer, or financial planner. The information presented reflects our analysis of publicly available data and should not be relied upon as a basis for investment decisions. Precious metals investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. Always consult a qualified financial advisor before making investment decisions. For more information about Sound Money's products and services, visit sound.money.

- gold

- silver

- precious-metals

- federal-reserve

- warsh

- fomc

- monetary-policy

- dca

- weekly-update