Jerome Powell chaired his final FOMC meeting. He held rates. He said nothing that moved markets. Gold fell 3.6% -- then found its floor. Warsh is on his way. What does a hawkish handover actually mean for the people stacking every month?

The Hawkish Handover: Gold Found Its Floor When Powell Said Nothing

Sound Money Weekly | May 4, 2026

The Hook

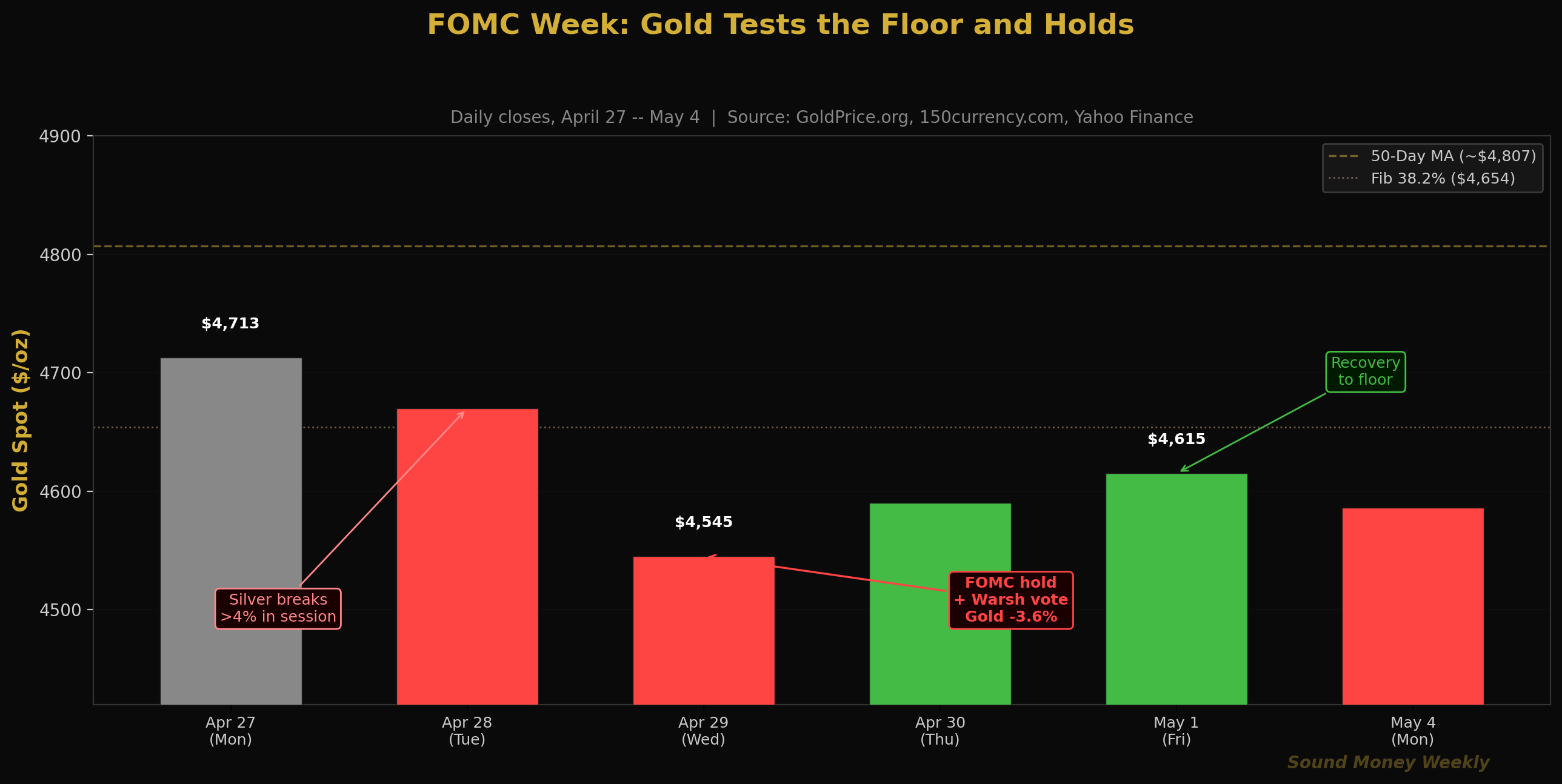

The market wanted a signal on Wednesday, April 29. It did not get one.

Jerome Powell stood at his final press conference as Federal Reserve Chair, held rates at 3.50-3.75% as expected, and declined to offer any conditional language about rate cuts -- no Hormuz clause, no oil price threshold, no hint of when the ceiling might lift. The WSJ's live coverage summarized the outcome simply: "Central Bank Holds Rates Steady." Powell also announced he would remain on the Fed Board as a governor after his term as chair expires May 15 -- a quiet signal that the institution intends continuity even as leadership changes.

Gold, which had opened the week at $4,713, fell 3.6% to approximately $4,545 on Wednesday. Silver dropped more than 4% in a single session on Tuesday before the FOMC decision even landed, then another 1.4% on Wednesday. By Friday, gold had recovered to $4,615. This morning it opened at approximately $4,586.

The price action tells the story cleanly: no cuts signal = ceiling holds = short-term pressure. Then the floor catches it.

The floor has held through every test since the March flash crash. The $4,361 Fibonacci 50% level has not been seriously threatened since late March. Gold at $4,615 is 17.7% below the January all-time high and 42% above where it was a year ago. Every major bank still targets $5,400 to $6,300 by year-end. Not one has cut its forecast.

Meanwhile, the Federal Reserve is about to have a new chair for the first time in eight years. Kevin Warsh cleared the Senate Banking Committee on April 29 -- the same day as Powell's final meeting -- and the full Senate vote is expected the week of May 11. Warsh could be the Fed Chair before Powell's term even expires on May 15.

The surface story is: hawkish hold, gold pulls back, neutral recovery. The deeper story is about what gold has accumulated through this entire transition -- and what it stands to gain when the ceiling eventually lifts.

The Week in Full

Monday, April 28 (day before FOMC): Gold was steady near $4,670. Silver was the more dramatic story. In a single session, silver dropped more than 4% -- triggering the daily scan's threshold alert. The trigger was not silver-specific news. It was the rate-expectations math: as the market anticipated a neutral (rather than dovish) Powell press conference, traders sold silver first. Why silver before gold? More on that below.

Wednesday, April 29 (FOMC + Warsh vote): A historic confluence of events. The Fed held rates at 3.50-3.75% -- the seventh consecutive hold in the current cycle. Powell's statement contained no conditional language on cuts. Gold fell from $4,670 to approximately $4,545 intraday, a drop of roughly 3.6%. Simultaneously, the Senate Banking Committee voted 13-11 along party lines to advance Kevin Warsh's nomination. All 13 Republicans supported it; all 11 Democrats opposed it, with Democratic senators including Elizabeth Warren warning that Warsh would operate as a "sock puppet" for a president who has repeatedly called for lower rates.

Thursday, April 30 (Q1 GDP and Warsh context): The market digested both events. Gold found support near $4,590 as investors recognized that the neutral language, while disappointing for near-term rate cut hopes, does not change the structural picture.

Friday, May 1: Gold closed at $4,615. A clean recovery of roughly $70 from Wednesday's intraday low. The Fibonacci 0.382 support at $4,654 drew buyers; the floor held.

Weekend / Monday, May 4: Gold hovering near $4,586 as the week opens in quiet mode ahead of the full Senate Warsh vote, scheduled for the week of May 11.

Why Silver Dropped Like a Tech Stock

Before the FOMC decision even arrived, silver fell more than 4% in a single session. To most casual observers, this looks like silver tracking gold. It isn't. Silver moved faster and harder because it carries two simultaneous identities -- and both went against it at the same moment.

Silver is a monetary metal. When real yields rise (or cut expectations fall), investors reduce precious metals exposure. That's the same logic that pressures gold. But silver also carries an industrial identity. It is in solar panels, EVs, semiconductors, and AI server components. When "higher for longer" rates take hold, industrial demand expectations soften alongside the monetary bid. Gold has only the monetary channel. Silver has both working against it simultaneously.

There is a counterintuitive twist to the solar angle worth understanding. Silver briefly surpassed $100 per ounce in January 2026 -- it even briefly touched $117. That price spike triggered something unexpected: solar manufacturers began a serious "thrifting" effort, swapping silver paste for copper in photovoltaic cells where technically feasible. By 2026, this substitution is accelerating. The industry is quite literally redesigning solar panels to use less silver.

And yet: the Silver Institute still projects a sixth consecutive annual supply deficit in 2026. Less silver per panel does not automatically mean more supply. What it means is that global solar demand is so enormous -- and growing so fast -- that even with active substitution efforts, manufacturers cannot outrun the fundamental gap between mine supply and aggregate demand. The deficit shrinks but does not close.

This is one of the less understood dynamics in silver: the industrial sector is simultaneously its biggest growth driver and its most active counter-pressure. When silver gets expensive enough that the industry redesigns around it, that redesign effort is itself evidence of how deeply embedded silver demand has become.

Under the Hood: Technical View and the Warsh Era

Gold's Technical Position

After the week's volatility, gold at $4,615 sits:

- 17.7% below the January $5,608 all-time high

- 12.6% above the March 23 flash-crash low of $4,098

- Just below the Fibonacci 0.382 level at $4,654 (former resistance, now support)

- Meaningfully below the 50-day moving average at ~$4,807

| Level | Price | Note |

|---|---|---|

| 50-Day MA (resistance) | ~$4,807 | First major overhead target |

| Fib 0.382 (support) | $4,654 | Testing as support post-FOMC |

| Current | ~$4,615 | Between the two levels |

| Fib 0.500 (major support) | $4,361 | Structural floor; held through all March tests |

| 200-Day MA | ~$4,200 | Long-term bull/bear line |

The pattern is consistent with what we observed in March: gold tests support, institutional buyers step in, the floor holds. The question is not whether the correction is over -- it broadly is, above $4,361. The question is what the near-term catalyst looks like. That answer is increasingly tied to one word: Warsh.

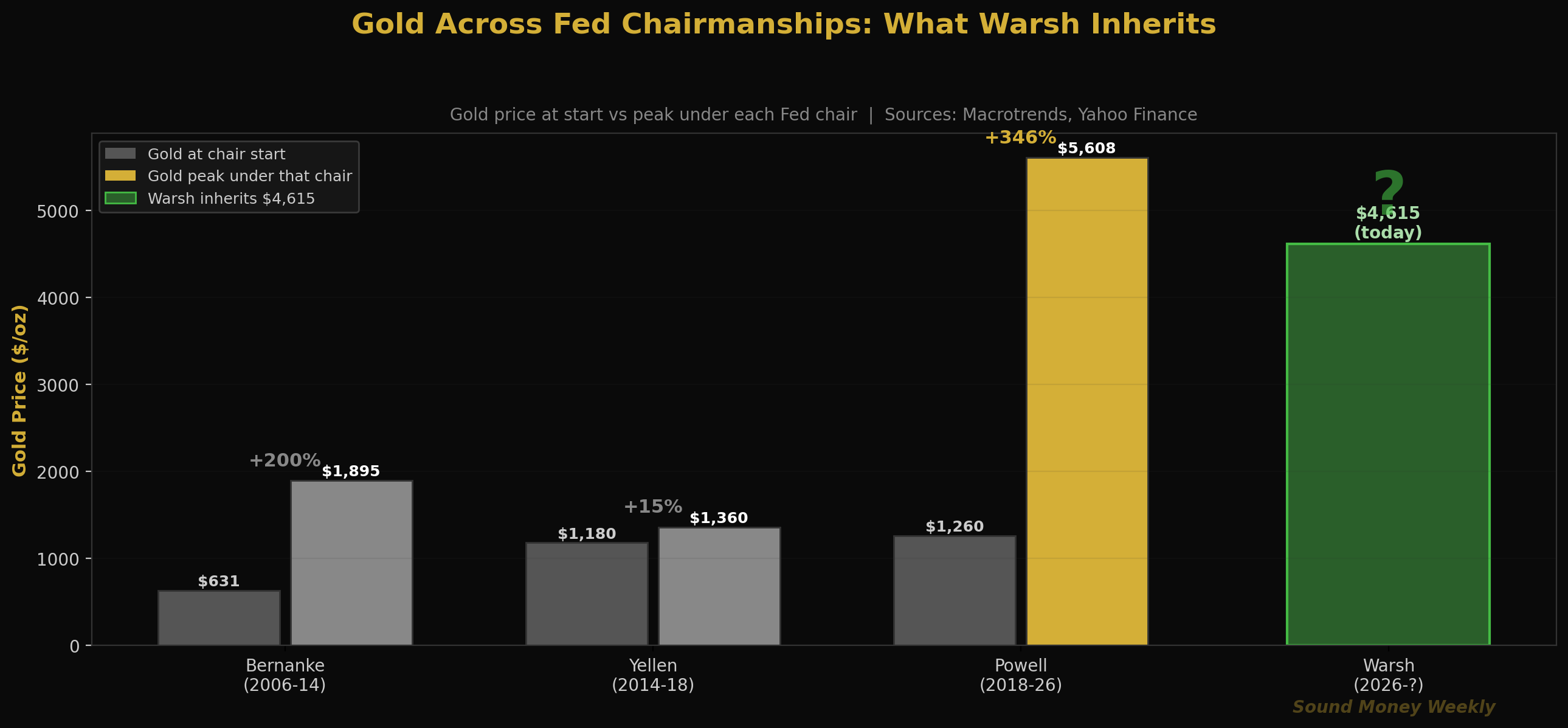

What Gold Has Done Through Every Fed Era

Here is a perspective most FOMC commentary misses. Gold rose approximately 200% during Bernanke's tenure as the Fed expanded its balance sheet through QE. Gold rose modestly during Yellen's tenure as the tightening cycle began. Under Powell -- who inherited $4.5 trillion in Fed assets, oversaw their expansion to $9 trillion during COVID, and then managed the most aggressive rate hiking cycle since Volcker -- gold rose 346%: from $1,260 to a peak of $5,608.

Kevin Warsh inherits a Fed at $4,615 gold. He inherits $39 trillion in federal debt. He inherits $1.1 trillion in annual debt service costs that now exceed the entire defense budget. And he inherits the structural reality that the rate path which brought gold to $5,608 -- low rates, fiscal expansion, balance sheet growth -- has not been permanently reversed. It has been temporarily paused.

Warsh has advocated for balance sheet reduction and a "regime change" in Fed communication. He wants fewer press conferences, less forward guidance, and a smaller Fed footprint. What he has not proposed -- and what no serious economist believes is feasible -- is a solution to a $39 trillion debt load that requires structural monetization to service.

The hawkish handover is real. The structural floor is more real.

The DCA Math at $4,615

Gold at $4,615 this morning. The math has been consistent since March -- each weekly purchase is acquiring more metal at a discount to the January all-time high.

| Entry Point | Price | Oz per $200 | Value at Goldman $5,400 |

|---|---|---|---|

| January ATH | $5,608 | 0.03566 oz | $192 |

| Today | $4,615 | 0.04333 oz | $234 |

| March low | $4,098 | 0.04881 oz | $264 |

At $4,615, a $200 monthly purchase acquires 0.04333 ounces -- 21.5% more metal than the same purchase at January's all-time high. Over 12 months of consistent stacking at this price, you accumulate approximately 0.520 ounces. At Goldman's $5,400 year-end target, that is $2,808 -- a 17% return on $2,400 invested. At J.P. Morgan's $6,300, it is $3,278 -- a 36.6% return.

The people who have consistently stacked through March's flash crash, through the ceasefire bounce, through Powell's final FOMC, and through this week's hawkish neutral statement have accumulated gold at an average cost well below today's price. The people waiting for the ceiling to lift before resuming accumulation will pay a different entry price when it does.

The Hartford Funds research remains the definitive statement on the cost of timing: missing the 10 best trading days in a 30-year period cuts total returns roughly in half. Those best days -- the ceasefire bounce, the DOJ probe drop, the Hormuz reopening when it comes -- do not wait for anyone to make a decision. The winners in this game are always in the game.

What It Means

Here is the plain-English version.

The ceiling held, and gold found its floor. Powell's neutral exit language was the worst realistic outcome for near-term gold -- no cut signals, no conditions, no hope. Gold fell 3.6%. Then it bounced. The floor between $4,550 and $4,620 has held through every test since the ceasefire bounce in early April. The structure says: the correction phase from the January high is resolved. What remains is the wait for the next catalyst.

Silver's -4% session is not a silver story. It is a rate sensitivity story. Silver is, as the Paul Harvey script put it, "a rate-sensitive metal wearing an industrial costume." When rate cut expectations contract, silver gets sold first because it carries both the monetary and industrial channels simultaneously. The structural deficit story -- sixth consecutive annual shortfall -- has not changed. But silver's short-term price action is more volatile than gold's because the market has more reasons to sell it quickly.

Warsh is not the bearish catalyst most people assume. Yes, he is a hawk. Yes, he wants balance sheet reduction. Yes, he criticized the Fed's 2021-22 policy errors. But the market's reaction to the DOJ probe being dropped two weeks ago -- gold going UP when Warsh's confirmation was de-risked -- told us something important: what markets feared was not a credible hawkish Fed. It was an incredible one. Warsh being confirmed as a genuinely independent chair is, on balance, a stabilizing signal for institutional credibility. Sound money does not fear a credible Fed.

The structural case compounds quietly. US debt service exceeds $1 trillion annually for the first time in history. Central banks are on pace for their 18th consecutive year of net gold buying. Silver's supply deficit is entering year six. The AI infrastructure buildout is beginning to drive a grid expansion that analysts now describe as the largest since the post-WWII electrification push -- and grid expansion means transformer copper, transmission silver, and physical metals demand that no monetary policy can create or destroy.

This is not a recommendation. We do not know when the Hormuz situation resolves, or when Warsh's first FOMC meeting signals a direction. We do know that gold has delivered 10.9% annualized returns since 2000 with no negative rolling 20-year period. We know every major bank maintains $5,400-$6,300 year-end targets. And we know that at $4,615, every $200 purchase acquires 21.5% more metal than the same purchase at the January high.

What We're Watching

Week of May 11: Full Senate Warsh vote. The Banking Committee advanced him on April 29. The full Senate is scheduled to vote the week of May 11. If confirmed, Warsh becomes Fed Chair before Powell's May 15 term expires. Watch the vote for any procedural surprises -- a blocked confirmation would create Fed leadership ambiguity that historically drives gold higher.

May 13: April CPI. The single most important data point in the near term. If Brent crude has continued its modest retreat from $112 (at the height of the conflict) toward $90-95, the April CPI should show a meaningful drop in the energy component. A headline print below 2.8% would trigger immediate rate-cut repricing and a gold rally. A print above 3.3% extending the March level would reinforce the hawkish ceiling.

May 15: Powell departs, Warsh (likely) takes over. The institutional handover. Watch for Warsh's first public statement as chair and any signals about press conference frequency, forward guidance, or balance sheet trajectory. His confirmation hearing comments -- fewer press conferences, less forward guidance -- suggest a more opaque Fed. Less transparency typically means more uncertainty, which historically supports gold.

Iran. The ceasefire has held through this FOMC cycle. Brent crude has retreated modestly. The April 22 Islamabad talks produced progress but no permanent deal. If any Hormuz reopening announcement precedes a May FOMC meeting, the compound effect -- lower oil, lower CPI, rate cut window opens -- would be gold's strongest near-term catalyst.

The AI grid story. US data centers consumed 176 terawatt-hours of electricity in 2023. Projections now show 325 to 580 terawatt-hours by 2028. That means a massive rebuild of transmission infrastructure -- transformers, cables, substations. Most market commentary on AI focuses on semiconductors. The overlooked story is that this is also the largest physical metals demand signal since the post-war electrification era. Silver is in the conductors. Copper is in the transformers. The grid does not get rebuilt with software.

Until Next Week

Jerome Powell served as Federal Reserve Chair for eight years. Under his tenure, gold rose 346% -- from $1,260 to a peak of $5,608. He oversaw QE expansion to $9 trillion, a zero-rate era that lasted three years, the most aggressive hiking cycle since Volcker, and a precious metals rally that produced the metal's best 24-month performance in over four decades.

He left without saying a word about what comes next for rates.

Kevin Warsh inherits this at $4,615. He inherits $39 trillion in debt, $1.1 trillion in annual interest, a silver market in its sixth consecutive deficit year, and a gold market that has priced every geopolitical, fiscal, and monetary risk for the better part of two years. Whether he is hawkish or centrist, whether he holds rates or cuts, whether he reduces the balance sheet or pauses -- the structural arithmetic does not change.

The dollar on the OG image for this article is worn and weathered. It has been used, folded, traded, and lost value to every asset class that has kept pace with inflation. Gold is not worn. It does not fold. And the people who have been stacking $200 worth of it every month since the January high now own 21.5% more ounces per dollar than they would have if they had waited for clarity.

The winners in this game are always in the game. See you next Monday.

Sound Money offers fractional gold and silver ownership at whole-ounce pricing -- no minimums, no premiums. Learn more at sound.money.

Disclaimer: This content is provided by Sound Money for educational and informational purposes only. Nothing published here constitutes investment advice, financial advice, trading advice, or any other form of professional advice. Sound Money is not a registered investment advisor, broker-dealer, or financial planner. The information presented reflects our analysis of publicly available data and should not be relied upon as a basis for investment decisions. Precious metals investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. Always consult a qualified financial advisor before making investment decisions. For more information, visit sound.money.

- gold

- silver

- precious-metals

- federal-reserve

- warsh

- fomc

- monetary-policy

- silver-industrial

- weekly-update