Everyone expected inflation to cool in April. The opposite arrived. Here is what gold did -- and what it tells you about the structure beneath the price.

The Wrong CPI: Gold Tests Its Floor as Inflation Hits a Three-Year High

Sound Money Weekly | May 18, 2026

The Hook

The consensus was clear going into last week. March's 3.3% CPI print was an energy shock. Oil had retreated from $112 toward $90. Gasoline prices were coming down. April's CPI would reflect that retreat. Rate-cut expectations would revive. Gold would break through $4,807.

On Tuesday, May 12, the Bureau of Labor Statistics published the April CPI report.

It came in at 3.8%.

Not the cooling print the market was pricing. A three-year high. The worst headline CPI since the early months of 2023. The April PPI released the following day was also hot, confirming upstream pricing pressure was still building. Markets completely priced out 2026 rate cuts in a single session, and began pricing in the possibility of a rate hike in 2027.

On the same afternoon that the hot CPI was being processed, the Senate confirmed Kevin Warsh as Federal Reserve Chair 54-45 -- the first bipartisan element being Senator John Fetterman (D-PA) crossing the aisle -- confirming the new era of monetary management exactly as that management was handed the most challenging inflation environment in three years.

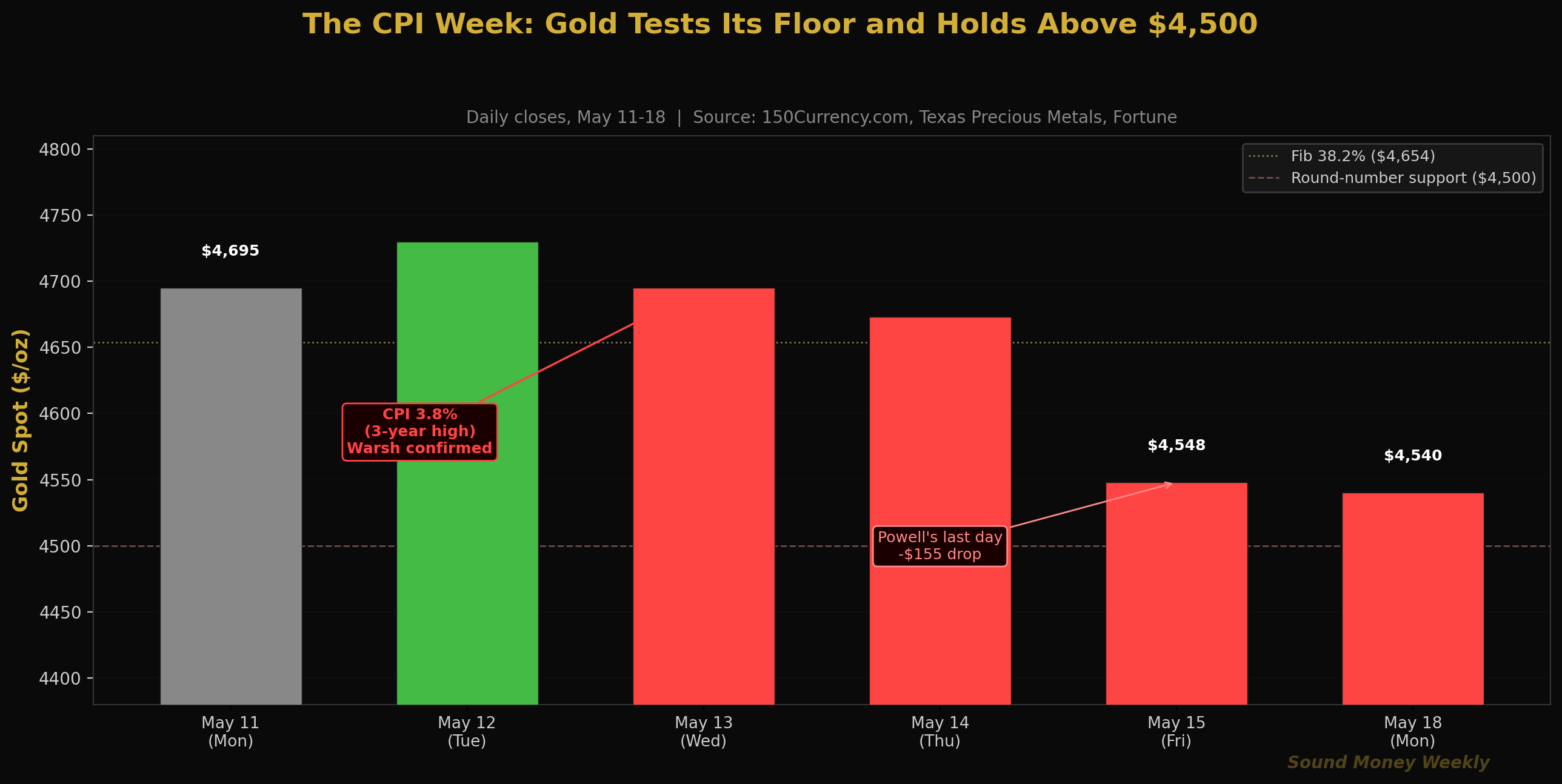

Gold fell. On May 15, Jerome Powell's final day as Fed Chair, gold dropped $155 to $4,548. By the weekend, it sat at $4,534. This morning it opened at $4,540.

Here is what that floor test reveals.

The Week in Full

Monday-Tuesday, May 11-12: Gold opened the week at $4,695, continuing the steady recovery from the FOMC-driven low of $4,545. By Tuesday morning, ahead of the CPI release at 8:30 AM, silver briefly surged more than 5% intraday and gold spiked above $4,730 on short-covering and positioning ahead of what markets expected to be a cooler print. Within hours of the actual number dropping, the reversal was sharp.

Wednesday, May 13 (the pivot): April CPI: 3.8%. The combination of persistent energy costs, service inflation, and residual import tariff pass-through produced the hottest consumer price data since early 2023. On the same afternoon, the Senate voted 54-45 to confirm Kevin Warsh, installing a known hawk at the Fed at the precise moment when the data was screaming that tighter policy was justified. Gold closed at $4,699 -- nearly flat for the day -- as the market absorbed both pieces of news simultaneously.

Thursday-Friday, May 14-15: The full implications settled in. Gold dropped $155 on Friday, May 15 -- Jerome Powell's last day. The symbolic weight of the transition, combined with the hawkish macro repricing, produced the week's largest single-session move. Gold at $4,548 was testing support levels not seriously threatened since the ceasefire bounce in early April.

Weekend / Monday, May 18: Gold stabilized near $4,534-$4,540 over the weekend and opened this morning at $4,540 -- essentially unchanged from the Friday close. The floor, for now, is holding.

The Inflation Story: Why 3.8% Was a Surprise

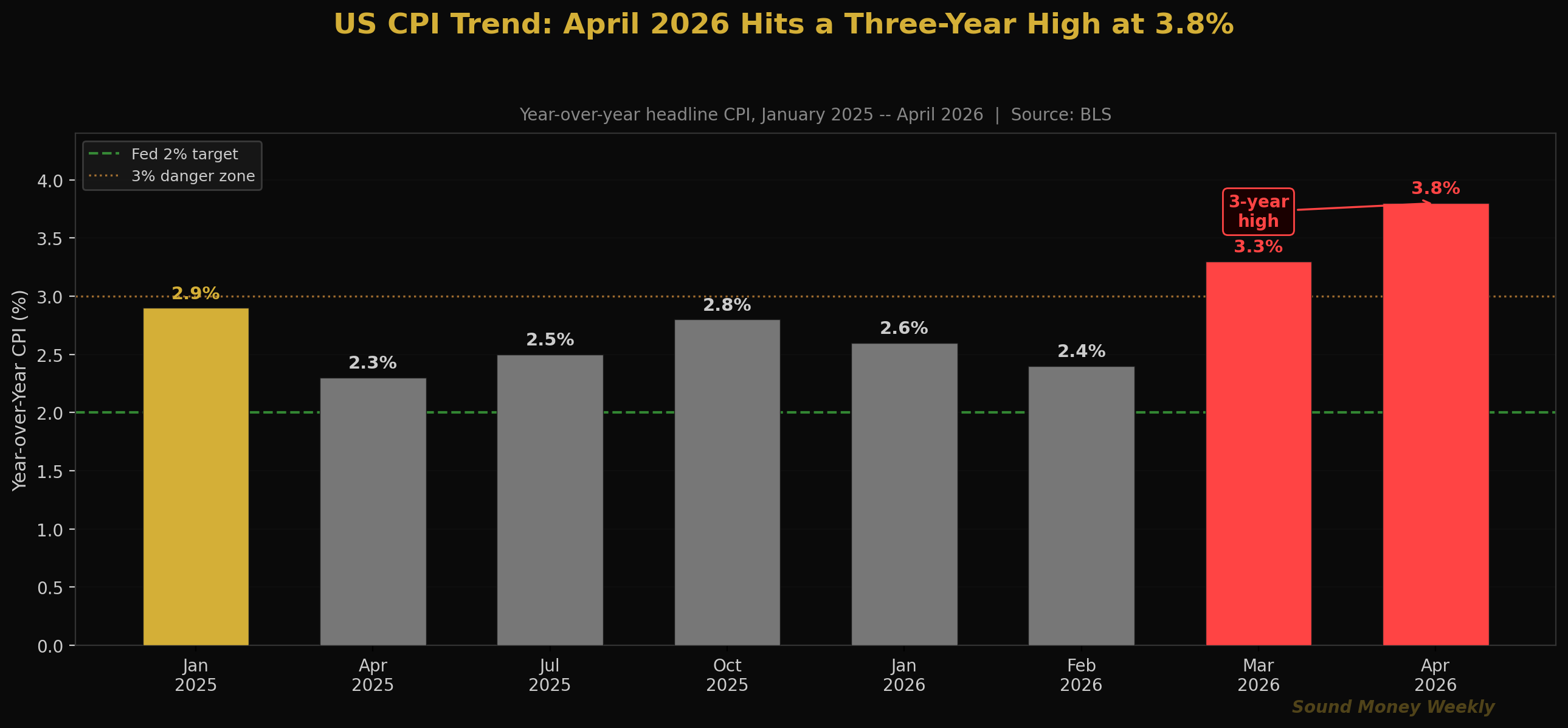

The CPI had been decelerating for most of 2025. By August 2025 it had reached 2.3%, the closest to the Fed's 2% target since pre-pandemic. Then the Iran conflict began, oil spiked, and by March 2026 the headline had climbed back to 3.3%.

The March print was alarming but explicable: energy. Brent crude had run from $67 to $112 in less than a month, and that oil price shock was always going to show up in March data. The thesis was: oil retreated. April would reflect that retreat. By May, inflation would be back on a downward path.

The thesis was wrong for two reasons. First, oil's retreat from $112 was slower than markets expected -- Brent is still in the $90-95 range, and pump prices lag crude moves by four to six weeks. Second, services inflation -- which the Fed watches more closely than energy -- has not cooperated. Shelter, medical services, and transportation all ran hot in April, reflecting underlying demand-side pressures that have nothing to do with oil.

The result: 3.8% headline, a 3-year high, and a Federal Reserve whose new chair is legally, institutionally, and philosophically positioned to respond with higher rates if inflation persists.

The India Angle Nobody Is Talking About

Here is a detail from this week that most inflation commentary missed entirely.

On May 13, India raised import duties on gold and silver from 6% to 15%. The stated rationale was to slow bullion imports and protect the Indian rupee, which had been weakening against the dollar.

Consider what that policy decision actually reveals. India is the world's second-largest gold consuming nation. When its government decides that gold imports are significant enough to influence the rupee's value -- significant enough to warrant a nearly 150% increase in tariffs -- it is making an implicit admission: gold and the rupee are in direct competition for the same store-of-value demand. Indians converting rupees to gold are, from the government's perspective, choosing to hold an asset that is not the currency.

That is not a trivial admission. Governments do not tax things they are not afraid of. When a major government raises gold tariffs to "arrest a currency slide," it is confirming, in policy language, that gold is winning a competition against the local currency. For stackers, the takeaway is not "gold is restricted in India." It is: "the world's second-largest gold market's government just told you what gold does."

Under the Hood: The Technical Picture at $4,540

Gold at $4,540 this morning is:

| Level | Price | Status |

|---|---|---|

| 50-Day MA | ~$4,807 | Overhead resistance; not in play near-term |

| Fib 0.382 | $4,654 | Broken on the Friday selloff |

| Current | $4,540 | Testing the zone between two Fibonacci levels |

| Fib 0.500 | $4,361 | The structural floor; held through all of March |

| Round-number support | $4,500 | Psychological level; holding so far |

| 200-Day MA | ~$4,200 | Long-term bull/bear line; well below |

The Friday drop broke through the Fibonacci 0.382 support at $4,654, which has been acting as a floor since the ceasefire bounce. Gold now sits between $4,654 (broken) and $4,361 (the May structural floor). The $4,500 level is the first psychological support; the $4,361 Fibonacci 0.500 remains the structural test.

The key question technically is whether the Friday break was a clean structural deterioration or a news-driven spike-low (like the March 23 flash crash to $4,098, which recovered quickly). Gold held above $4,500 through the weekend and opened Monday at $4,540 -- which is consistent with the spike-low pattern rather than structural deterioration.

Warsh's first official action at the Fed will be closely watched for signals about June. If his initial communications lean pragmatic rather than hawkish, markets could reverse the rate-hike pricing and gold could recover toward $4,654 quickly.

The DCA Math at $4,540

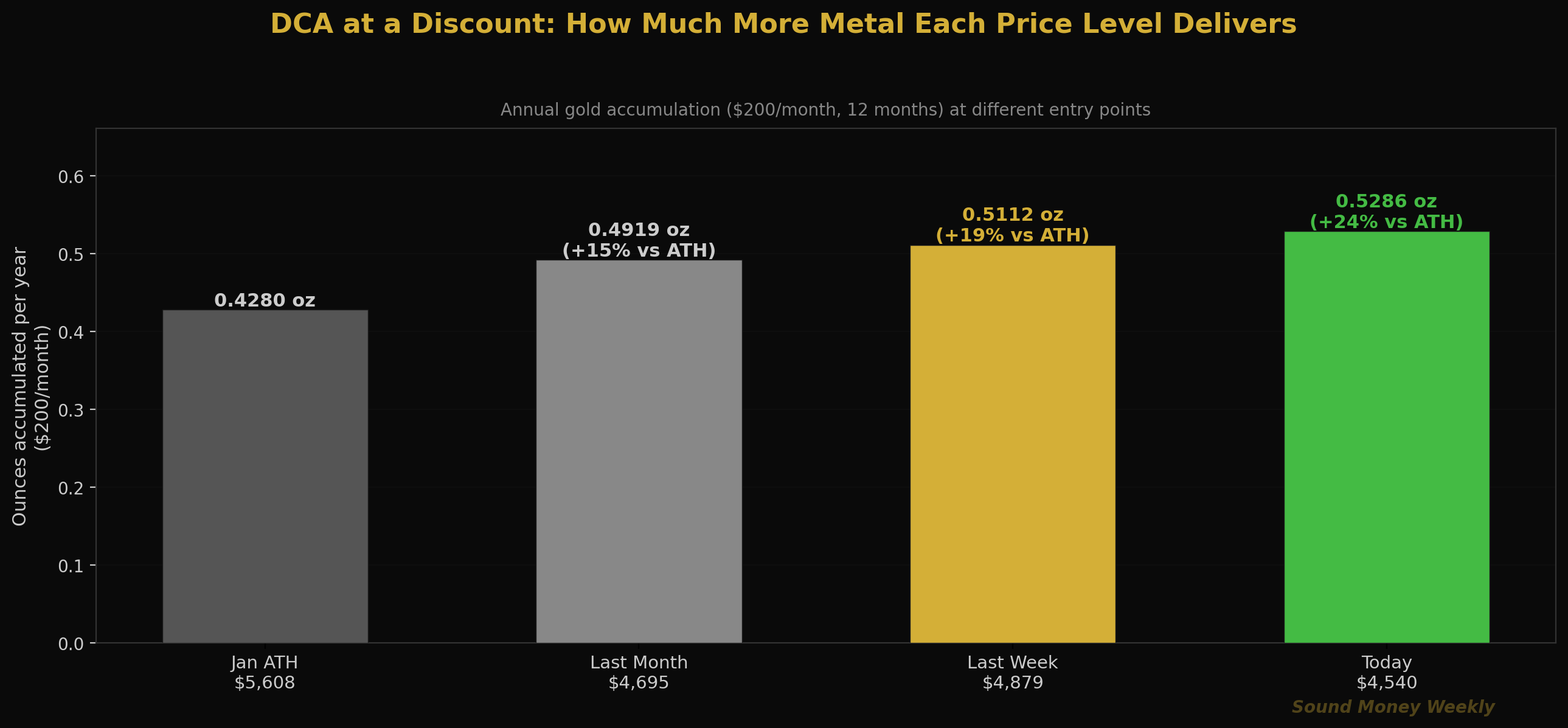

The floor test creates an important DCA math update. At $4,540, the accumulation advantage over the January all-time high is now 23.4%:

| Entry Point | Price | Oz per $200/mo | Annual total (12 mo) |

|---|---|---|---|

| January ATH | $5,608 | 0.03566 oz | 0.428 oz |

| Today | $4,540 | 0.04405 oz | 0.529 oz |

The consistent stacker at $200/month buying at today's prices will accumulate 0.529 ounces over 12 months -- 23.6% more than the same program at the January high. At Goldman's $5,400 year-end target, that stack is worth $2,857 -- a 19% return on $2,400 invested. At J.P. Morgan's $6,300, it is $3,333 -- a 38.9% return.

Here is the structural irony of this week: the same CPI print that is temporarily weighing on gold's price by removing rate-cut hopes is also confirming the thesis for holding gold. At 3.8% YoY, inflation is running more than 90 basis points above the Fed's 2% target, for the fifth consecutive year. The dollar's purchasing power continues to erode against everything -- including gold. The $4,540 price represents more ounces per dollar, not a weaker argument for owning those ounces.

The people who have been stacking $200/month through March's flash crash, through the ceasefire bounce, through the Powell-to-Warsh transition, and through this week's CPI shock have accumulated gold at an average cost well below today's price. The people who paused because of CPI uncertainty are now considering whether to restart at $4,540 -- exactly the price that would have seemed like a screaming entry point three months ago.

The winners in this game are always in the game.

What It Means

Here is the plain-English version.

April CPI at 3.8% is a setback for the near-term rate-cut thesis -- not the structural thesis. The rate-cut narrative was the mechanism markets were using to justify gold above $5,000. That mechanism is now off the table for 2026. The structural argument -- 18 consecutive years of central bank net buying, the sixth silver supply deficit, $39 trillion in US debt, and an inflation rate that has not sustained the Fed's 2% target in five years -- is not changed by one month of CPI data.

Gold held above $4,500 through a 3-year CPI high and a hawkish Fed confirmation. That is not weakness. That is the floor showing what it is made of. In March, gold held above $4,361 through a 27% intraday drawdown from the ATH. In May, gold held above $4,500 through the worst inflation print in three years and a simultaneous hawkish chair installation. The structure is durable.

The India import duty hike is a structural signal. No government taxes an asset into irrelevance. When the Indian government raises gold tariffs to defend the rupee, it is confirming the competition between gold and paper currency at a policy level. That competition is not unique to India. Every government running persistent deficits faces it. Every government with a weakening currency faces it. The tariff is not bearish for gold. It is evidence of gold's relevance.

Warsh's first statements matter more than the CPI print. The hot CPI is a constraint on what he can do, not an instruction for what he will do. His first communications as chair -- scheduled for later this month -- will reveal whether he intends to lean hawkish immediately or signal patience while the Iran situation remains unresolved. A patient signal could reverse the rate-hike pricing and give gold an immediate catalyst. A hawkish signal would extend the ceiling but confirm the floor.

This is not a recommendation. We do not know where gold goes next week or next month. We do know it has produced a 10.9% annualized return since 2000, that central banks have been net buyers for 18 consecutive years, and that at $4,540 each monthly purchase acquires 23.6% more ounces than it did at the January high. The data makes the case. We just report it.

What We're Watching

Warsh's first public communications. The new Fed Chair's initial statements on policy direction, press conference cadence, and balance sheet trajectory are the most important near-term catalyst for gold in either direction. A pragmatic, conditional tone would be meaningfully bullish. A pure-hawkish tone would extend the ceiling.

May FOMC (no meeting this week -- next meeting is June 10-11). The June meeting is now the focus. Markets have moved toward pricing no cuts in 2026 and possible hikes in 2027. Any data between now and June 11 that complicates the 3.8% CPI picture (PCE inflation, jobs data) will move that pricing.

India demand data. With import duties at 15% (up from 6%), smuggling typically rises and official demand falls. The medium-term effect on gold price is ambiguous: less official Indian demand is slightly bearish, but government restriction of gold is itself a structural signal that reinforces long-term conviction. Watch GJEPC trade data in coming months.

The $4,361 level. The Fibonacci 0.500 retracement -- the structural floor that has held since the March selloff. Gold has closed above it for 45 consecutive sessions. If it breaks, the correction has re-entered a more serious phase. If it holds through the Warsh transition, the bull structure remains intact.

Iran. The ceasefire is still technically in force. If Hormuz reopens meaningfully, oil drops toward $80, inflation expectations fall, and rate-cut pricing revives. That is still the single most powerful catalyst available for a gold recovery -- and it has nothing to do with the Fed.

Until Next Week

Every week that gold holds its structural floor through a new headwind builds the case that the floor is real. This week the headwind was a 3-year CPI high, a hawkish Fed installation, and markets pricing out every rate cut in 2026. Gold fell $155. Then it stabilized.

The Iran conflict is still live. The ceasefire is still fragile. Central banks are still buying gold for the 18th consecutive year. US debt service still exceeds the defense budget. The silver supply deficit is still entering its sixth year.

A 3.8% CPI print does not change any of those facts. It changes the rate-cut mechanism but not the structural argument. The dollar bill shown on gas station signs across America still buys less of everything this month than it did last month. Gold has historically been one of the most reliable ways to hold purchasing power across decades.

At $4,540, consistent stackers are acquiring 23.6% more gold per dollar than they did at January's high. The thesis compounds quietly while headlines obsess over the near-term signals.

The winners in this game are always in the game. See you next Monday.

Sound Money offers fractional gold and silver ownership at whole-ounce pricing -- no minimums, no premiums. Learn more at sound.money.

Disclaimer: This content is provided by Sound Money for educational and informational purposes only. Nothing published here constitutes investment advice, financial advice, trading advice, or any other form of professional advice. Sound Money is not a registered investment advisor, broker-dealer, or financial planner. The information presented reflects our analysis of publicly available data and should not be relied upon as a basis for investment decisions. Precious metals investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. Always consult a qualified financial advisor before making investment decisions. For more information, visit sound.money.

- gold

- silver

- precious-metals

- inflation

- cpi

- warsh

- federal-reserve

- india

- weekly-update